$341 Million Deployed - and not a dollar of capital lost

Share this post

Since launching LCIM's latest fund in 2021, the Lambert Capital Property Credit Fund has funded over $341 milion in loans to Australian property developers.

In private credit, milestones tend to be measured in dollars lent. The number that actually matters is what happened to investor's capital along the way.

The Lambert Capital Property Credit Fund (LCPCF) has now deployed approximately $341 million in loans since its current fund commenced in July 2021; part of a lending history dating back to 2009. Across that entire period, first mortgage investors have not experienced a single dollar of capital loss, while receiving consistent risk adjusted returns well in excess of the fund's 7-10% pa target range.

With the YTD IRR of 10+% pa, this reflects both careful loan selection and a portfolio structured to generate cash rather than rely on long dated exits.

Private construction lending often leads with speed and flexibility. Both have their place; but neither substiututes for sound judgement and disiplined deal structuring.

Most projects don't fail because the location was wrong or the market moved against them. Problems tend to emerge when the capital structure, loan timing and the developers experience aren't properly aligned. At Lambert Capital, that alignment is where the work begins.

Structure over speed

Lambert Capital provides senior debt facilities of approximately $5 million to $25 million to experienced real estate developers, primarily across metropolitan Melbourne and key markets in Victoria, New South Wales and Queensland. The average loan size currently sits at around $8.3 million; a deliberate focus on the mid-market segment where risk is more identifiable and manageable.

Most facilities are designed to run between 9 and 15 months. Shorter durations mean fewer variables accumulate over time. Contractor cashflow, presales managment, interest rate movements and market sentiment all compound with duration; keeping projects shorter limits that exposure.

A portfolio built for this market

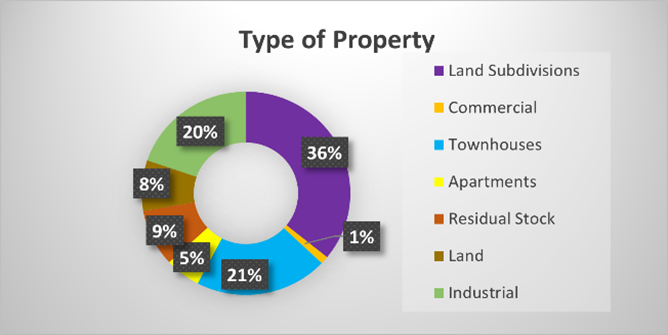

The current loan book spans residential construction, industrial warehouses and land subdivision, project types with defined completion timelines and identifiable exit paths. The fund's top five investments by loan size currently include a 72 lot residential land subdivision in Coral Cove, QLD, a 34 warehouse industrial construction in Melton, VIC and a 33 townhouse devlopment in Truganina, VIC.

The private credit and non-bank lending environment remains competitive, but Lambert Capital has continued to see strong deal flow; particularly in the $5 million to $20 million space. New enquiries have centred on affordable land subdivision in regional locations and townhouse developments in Melbourne's eastern suburbs, with repeat borrowers returning for subsequent project stages, in several cases ahead of their original schedule due to strong presales activity.

What the pipeline looks like

Lambert Capital currently holds approximately $44 million in mandates and issued term sheets, expected to settle over the next three to four months, with a further $57 million in transactions under assessment. Over the next six months, more than $30 million is expected to be deployed across existing loans and five to six new investments, at an anticipated IRR of aproximately 10% pa.

Several loans within the portfolio will also see scheduled reductions over the next one to three months via presale proceeds; providing liquidity to fund ongoing construction drawdowns and new sttlements without cash drag.\

What the number represents

Three hundred and forty-one million dollars is not a figure about scale for its own sake. Lambert Capital operates as a boutique specialist lender; experienced, selective and focused. It is the outcome of consistent underwriting decisions made across hundreds of individual loans over more than 15 years.

For developers, that track record means predicatble access to funding from a team, that understands how projects actually work. For investors, it means a fund tht has consistently delivered above its target range wihtout comprimising the capital they've entrusted to it.

That expertise translates into a broad range of funding solutions; construction finance, site acquisition and residual stock facilities, tailored to experienced developers who need a lender that actually understands their world.

Lambert Capital sits down with you, understands what your trying to achieve and gives you a straight answer on what can be delivered and when.

In property credit, process eventually shows up as performance. The numbers reflect that.

To find out how we can help finance your next project, please reach out directly to:

Olivia 0481 775 991

Gabrielle 0497 930 587

Peter Daicos PDaicos@LambertCapital.com.au

Recent Articles